Полная версия:

Economics

black knight see TAKEOVER BID.

black market an ‘unofficial’market that often arises when the government holds down the price of a product below its equilibrium rate and is then forced to operate a RATIONING system to allocate the available supply between buyers. Given that some buyers are prepared to pay a higher price, some dealers will be tempted to divert supplies away from the ‘official’ market by creating an under-the-counter secondary market. See BLACK ECONOMY.

board of directors the group responsible to the SHAREHOLDERS for running a JOINT-STOCK COMPANY. Often, boards of directors are made up of full-time salaried company executives (the executive directors) and part-time, nonexecutive directors. The board of directors meets periodically under the company chairman to decide on major policy matters within the company and the appointment of key managers. Directors are elected by rotation at the company ANNUAL GENERAL MEETING. See TWO-TIER BOARD, CORPORATE GOVERNANCE.

bond a FINANCIAL SECURITY issued by businesses and by the government as a means of BORROWING long-term funds. Bonds are typically issued for periods of several years; they are repayable on maturity and bear a fixed NOMINAL (COUPON) INTEREST RATE. Once a bond has been issued at its nominal value, then the market price at which it is sold subsequently will vary in order to keep the EFFECTIVE INTEREST RATE on the bond in line with current prevailing interest rates. For example, a £100 bond with a nominal 5% interest rate paying £5 per year would have to be priced at £50 if current market interest rates were 10%, so that a buyer could earn an effective return of £5/50 = 10% on his investment.

In addition to their role as a means of borrowing money, government bonds are used by the monetary authorities as a means of regulating the MONEY SUPPLY. For example, if the authorities wish to reduce the money supply, they can issue bonds to the general public, thereby reducing the liquidity of the banking system as customers draw cheques to pay for these bonds. See also OPEN MARKET OPERATION, BANK DEPOSIT CREATION, PUBLIC SECTOR BORROWING REQUIREMENT, SPECULATIVE DEMAND FOR MONEY, CONSOLS.

bonus scheme a form of INCENTIVE PAY SCHEME wherein an individual’s or group’s WAGES are based on achievement of individual or group output targets. Bonus schemes often provide for a guaranteed basic wage for employees. See PAY.

bonus shares SHARES issued to existing SHAREHOLDERS in a JOINT-STOCK COMPANY without further payment on their part. See CAPITALIZATION ISSUE.

boom a phase of the BUSINESS CYCLE characterized by FULL EMPLOYMENT levels of output (ACTUAL GROSS NATIONAL PRODUCT) and some upward pressure on the general PRICE LEVEL (see INFLATIONARY GAP). Boom conditions are dependent on there being a high level of AGGREGATE DEMAND, which may come about autonomously or be induced by expansionary FISCAL POLICY and MONETARY POLICY. See DEMAND MANAGEMENT.

borrower a person, firm or institution that obtains a LOAN from a LENDER in order to finance CONSUMPTION or INVESTMENT. Borrowers are frequently required to offer some COLLATERAL SECURITY to lenders, for example, property deeds, which lenders may retain in the event of borrowers failing to repay the loan. See DEBT, DEBTOR, FINANCIAL SYSTEM.

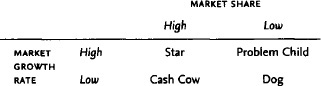

Boston matrix a matrix (developed by the Boston Consulting Group) for analysing product-development policy within a firm and the cash-flow implications of product development. Fig. 16 shows the matrix, which is used to identify products that are cash generators and products that are cash users. One axis of the matrix measures market growth rate: because the faster the growth rate for a product the greater will be the capital investment required and cash used. The other axis measures market share: because the larger the market share the greater will be the profit earned and cash generated. The market growth/share matrix encompasses four extreme product types:

(a) star products – those that have a high growth rate (so that they tend to use cash) and a high market share (so that they tend to generate cash). Star products are usually new products in the growth phase of the PRODUCT LIFE CYCLE.

(b) problem child products – those that have a high growth rate (and so tend to use cash) and a low market share (so that they tend to generate little cash). Problem products are frequently a cash drain but they have potential if their market share can be improved.

(c) cash cow products – those that have a low growth rate and a high market share (so that they tend to generate a lot of cash). Cash cows are usually mature products in the later phases of the product life cycle.

Fig. 16 Boston matrix. The matrix identifies cash generators and cash users.

(d) dog products – those that have a low growth rate and a low market share and tend to generate little cash. Dog products generally have little potential for future development.

It is important for any firm to have a balanced portfolio of mature ‘cash cow’ products, newer ‘stars’, etc., and to use the cash generated by cash cows to help the development of ‘problem children’ if its product development policy is to ensure the firm’s long-term survival. See PRODUCT PERFORMANCE, DIVERSIFICATION, PRODUCT-MARKET MATRIX.

bounded rationality limits on the capabilities of people to deal with complexity, process information and pursue rational aims. Bounded rationality prevents parties to a CONTRACT from contemplating or enumerating every contingency that might arise during a TRANSACTION, so preventing them from writing complete contracts.

boycott 1 the withholding of supplies of GOODS from a distributor by a producer or producers in order to force that distributor to resell those goods only on terms specified by the producer. In the past, boycotts were often used as a means of enforcing RESALE PRICE MAINTENANCE.

2 the prohibition of certain imports or exports, or a complete ban on INTERNATIONAL TRADE with a particular country by other countries.

brand the name, term or symbol given to a product by a supplier in order to distinguish his offering from that of similar products supplied by competitors. Brand names are used as a focal point of PRODUCT DIFFERENTIATION between suppliers.

In most countries, brand names and trade marks are required to be registered with a central authority so as to ensure that they are uniquely applied to a single, specific product. This makes it easier for consumers to identify the product when making a purchase and also protects suppliers against unscrupulous imitators. See INTELLECTUAL PROPERTY RIGHTS, BRAND TRANSFERENCE.

brand loyalty the continuing willingness of consumers to purchase and repurchase the brand of a particular supplier in preference to competitive products. Suppliers cultivate brand loyalty by PRODUCT-DIFFERENTIATION strategies aimed at emphasizing real and imaginary differences between competing brands. See ADVERTISING.

brand proliferation an increase in the number of brands of a particular product, each additional brand being very similar to those already available. Brand proliferation occurs mainly in oligopolistic markets (see OLIGOPOLY) where competitive rivalry is centred on PRODUCT-DIFFERENTIATION strategies, and is especially deployed as a means of MARKET SEGMENTATION. In the THEORY OF MARKETS, excessive brand proliferation is generally considered to be against consumers’ interests because it tends to result in higher prices by increasing total ADVERTISING and sales promotional expenses.

brand switching the decision by consumers to substitute an alternative BRAND for the one they currently consume. Brand switching may be induced by ADVERTISING designed to overcome BRAND LOYALTY to existing brands.

brand transference the use of an existing BRAND name for new or modified products. Brand transference or extension seeks to capitalize on consumers’ BRAND LOYALTY towards the firm’s established brands to gain rapid consumer acceptance of a new product.

brand value the money value of an established BRAND name. The valuation of a brand reflects the BRAND LOYALTY of consumers towards it, built up by cumulative ADVERTISING. See TAKEOVER.

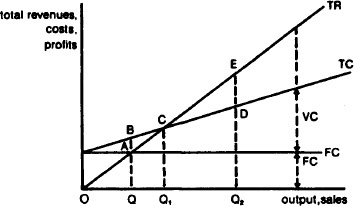

Fig. 17 Break-even. A supplier’s typical short-run costs and revenues. Fixed costs do not vary with output and so are shown as the horizontal line FC. Total cost comprises both fixed costs and total variable costs and is shown by line TC. Total revenue rises as output and sales are expanded and is depicted by line TR. At low levels of output like Q1 total costs exceed total revenues and the supplier makes a loss equal to AB. At high levels of output like Q2 revenues exceed costs and the supplier makes a profit equal to DE. At output Q1 total revenues exactly match total costs (at C) and the supplier breaks even.

break-even the short-run rate of output and sales at which a supplier generates just enough revenue to cover his fixed and variable costs, earning neither a PROFIT nor a LOSS. If the selling price of a product exceeds its unit VARIABLE COST, then each unit of product sold will earn a CONTRIBUTION towards FIXED COSTS and profits. Once sufficient units are being sold so that their total contributions cover the supplier’s fixed costs, then the company breaks even. If less than the break-even sales volume is achieved, then total contributions will not meet fixed costs and the supplier will make a loss. If the sales volume achieved exceeds the break-even volume, total contributions will cover the fixed costs and leave a surplus that constitutes profit. See Fig. 17.

Bretton Woods System see INTERNATIONAL MONETARY FUND.

bridging loan a form of short-term LOAN used by a borrower as a continuing source of funds to ‘bridge’ the period until the borrower obtains a medium- or long-term loan to replace it. Bridging loans are used in particular in the housing market to finance the purchase of a new house while arranging long-term MORTGAGE finance and awaiting the proceeds from the sale of any existing property.

broad money see MONEY SUPPLY.

brownfield location a derelict industrial site or housing estate that has been demolished and redeveloped to accommodate new industrial premises, often as part of a regional industrial regeneration programme. Compare GREENFIELD LOCATION. See REGIONAL DEVELOPMENT AGENCY.

budget (firm) a firm’s planned revenues and expenditures for a given future period. Annual or monthly sales, production, cost and capital expenditure budgets provide a means for the firm to plan its future activities, and by collecting actual data about sales, product cost, etc., to compare with budget the firm can control these activities more effectively.

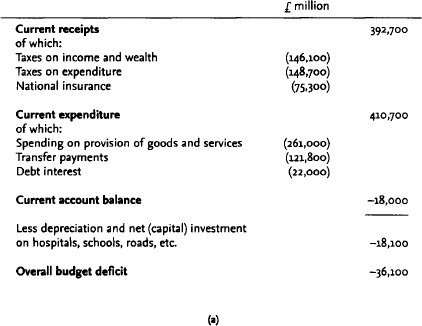

budget (government) a financial statement of the government’s planned revenues and expenditures for the fiscal year. The main sources of current revenues, as shown in Fig. 18 (a), are TAXATION, principally income and expenditure taxes, and NATIONAL INSURANCE CONTRIBUTIONS. The main current outgoings of GOVERNMENT EXPENDITURE are the provision of goods and services (principally wage payments to health, education, police and other public service employees), TRANSFER PAYMENTS (old-age pensions, interest payments on the NATIONAL DEBT, etc.) and social security benefits.

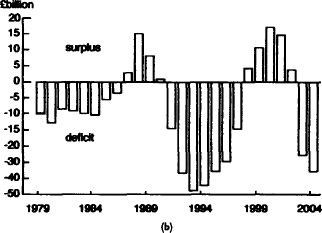

Fig. 18 Budget (government). (a) The UK budget for 2003/04. (b) UK budget deficits and surpluses, 1979–2004. Source: UK National Accounts, ONS (Blue Book), 2004.

The budget has two main uses: (a) it forms the basis of the government’s longer-term financial planning of its own economic and social commitments; (b) it is an instrument of FISCAL POLICY in regulating the level (and composition) of AGGREGATE DEMAND in the economy. A BUDGET SURPLUS (revenues greater than expenditures) reduces the level of aggregate demand. By contrast, a BUDGET DEFICIT (expenditure greater than revenues) increases aggregate demand. Fig. 18 (b) shows UK budget deficits (and surpluses) over the past two decades.

Recently (post 1997) the government has accepted that fiscal stability is an important element in the fight against INFLATION and UNEMPLOYMENT. To this end, fiscal ‘prudence’, specifically a current budget deficit within the European Union’s MAASTRICHT TREATY limits of no more than 3% of GDP (and an outstanding total debt limit of 60% of GDP), was endorsed as being a necessary adjunct to avoid excessive monetary creation of the kind that fuelled previous runaway inflation.

In fact, the government has gone further than this in adopting the so-called ‘golden rule’, which requires that the government should ‘aim for an overall budget surplus over the economic cycle’ (defined as 1998/99 to 2003/04, with some of the proceeds being used to pay off government debt to reduce outstanding debt eventually to 40% of GDP. Along the way it has introduced more rigorous standards for approving increases in public spending, in particular the ‘sustainable investment rule’, which stipulates that the government should borrow only to finance capital investment and not to pay for general spending. In addition, the government has announced it will ‘ring-fence’ increases in particular tax receipts to be used only for funding specific activities. For example, receipts from future increases in fuel taxes and tobacco taxes will be spent, respectively, only on road-building programmes and the National Health Service. See PUBLIC SECTOR BORROWING REQUIREMENT, PUBLIC SECTOR DEBT REPAYMENT, DEMAND MANAGEMENT, PUBLIC FINANCE.

budget (household) a household’s planned income and expenditure for a given time period. The household’s expenditure will depend upon its DISPOSABLE INCOME, and the THEORY OF CONSUMER BEHAVIOUR seeks to show how households, or consumers, allocate their income in spending on various goods and services. See CONSUMER EQUILIBRIUM.

budget deficit the excess of GOVERNMENT EXPENDITURE over government TAXATION and other receipts in any one fiscal year. See BUDGET (government). The operation of a budget deficit (deficit financing) is a tool of FISCAL POLICY to enable government to influence the level of AGGREGATE DEMAND and EMPLOYMENT in the economy. Such a policy was advocated by KEYNES in the 1930s to offset the DEPRESSION that occurred at that time. Opinion prior to this was that the government should operate a BALANCED BUDGET policy, allowing the economy to respond in its own way without government intervention. Keynes argued that government should intervene by deliberately imbalancing its budget in order to inject additional aggregate demand into a depressed economy and vice-versa.

Since the Second World War, most western governments have tended to operate a budget deficit to keep employment high and to promote long-term ECONOMIC GROWTH. This has been financed by increasing the PUBLIC SECTOR BORROWING REQUIREMENT (PSBR) through the issue of TREASURY BILLS and long-term bonds. This is acceptable as long as the economy is growing and the interest payments on such borrowings do not become disproportionate to the overall level of government expenditure. Government borrowing in excess of the amount required to promote long-term growth and effect counter-cyclical policies will ultimately result in INFLATION. Consequently, both the timing and magnitude of the expenditure over and above receipts is of crucial importance. In more recent times recognition that low inflation is necessary to secure low UNEMPLOYMENT has led to an acceptance of the need for ‘fiscal stability’. This has found expression, for example, within the European Union’s MAASTRICHT TREATY limits of a current budget deficit of no more than 3% of GDP and a total outstanding government debt limit of no more than 60% of GDP.

BUDGET SURPLUS is the opposite of the above whereby there is an excess of government receipts over expenditure. See AUTOMATIC (BUILT-IN) STABILIZERS, KEYNESIAN ECONOMICS, BUSINESS CYCLE, DEMAND MANAGEMENT.

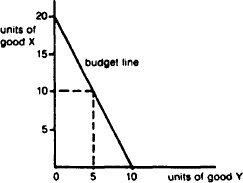

budget line or consumption possibility line a line showing the alternative combinations of goods that can be purchased by a consumer with a given income facing given prices. See Fig. 19. See also CONSUMER EQUILIBRIUM, REVEALED PREFERENCE THEORY, PRICE EFFECT.

budget surplus a surplus of TAXATION receipts over GOVERNMENT EXPENDITURE. Budget surpluses are used as an instrument of FISCAL POLICY to reduce the level of AGGREGATE DEMAND in the economy. See BUDGET (government), BUDGET DEFICIT, PUBLIC SECTOR DEBT REPAYMENT.

buffer stock a stock of a COMMODITY (copper, wheat, etc.) that is held by a trade body or government as a means of regulating the price of that commodity. An ‘official’ price for the commodity is established, and if the open-market price falls below this because there is excess supply at the fixed price, then the authorities will buy the surplus and add it to the buffer stock in order to force the price back up. By contrast, if the open-market price rises above the fixed price because there is an excess demand at the fixed price, then the authorities will sell some of their buffer stock in order to bring the price down. Through this mechanism the price of the commodity can be stabilized over time, avoiding erratic, short-term fluctuations in price.

Thus this mechanism attempts to avoid erratic short-term fluctuations in price. If the official price is set at too high a level, however, this will encourage over-supply in the long term and expensively accumulating stocks; while if the official price is set at too low a level, this will discourage supply in the long term and lead to shortages. See INTERNATIONAL COMMODITY AGREEMENT, PRICE SUPPORT, COMMON AGRICULTURE POLICY.

Fig. 19 Budget line. If a consumer has an income of £10 and the price of good X is 50 pence and the price of good Y is £1, he can buy 20 units of X or 10 units of Y, or some combination of both, for example 10 units of X and 5 units of Y. The slope of the budget line measures the relative prices of the two goods.

Building Societies Act 1986 a UK Act that gave BUILDING SOCIETIES new powers to augment their traditional business MORTGAGES by providing a range of other financial services for their customers. These include money transmission facilities (via cheque books), arranging insurance cover, obtaining traveller’s cheques and foreign currencies, managing unit trust pension schemes, buying and selling stocks and shares, and the provision of estate agency facilities. The Act has thus served to increase competition in the provision of financial services as between building societies, the COMMERCIAL BANKS and other financial institutions.

The Act also permits building societies to increase their capital resources and growth potential by incorporating themselves as JOINT-STOCK COMPANIES (as have the Abbey National and the Halifax), issuing shares and securing a stock exchange listing.

building society a financial institution that offers a variety of savings accounts to attract deposits, mainly from the general public, and which specializes in the provision of long-term MORTGAGE loans used to purchase property. In recent years, many of the larger UK building societies have moved into the estate agency business. Additionally, they have entered into arrangements with other financial institutions that have enabled them to provide their depositors with limited banking facilities (the use of cheque books and credit cards, for instance) and other financial services, a development that has been given added impetus by the BUILDING SOCIETIES ACT 1986.

Most notably, major building societies, such as the Abbey National and Halifax, have taken advantage of changes introduced by the BUILDING SOCIETIES ACT 1986 and the FINANCIAL SERVICES ACT 1986 and have converted themselves into public JOINT-STOCK COMPANIES, setting themselves up as ‘financial supermarkets’ offering customers a banking service and a wide range of personal financial products, including insurance, personal pensions, unit trusts, individual savings accounts (ISAs), etc. This development has introduced a powerful new competitive impetus into the financial services industry, breaking down traditional ‘demarcation’ boundaries in respect of ‘who does what’, allowing former building societies to ‘cross-sell’ these services and products in competition with traditional providers such as the COMMERCIAL BANKS, INSURANCE COMPANIES, UNIT TRUSTS, etc.

Building society deposits constitute an important source of liquidity in the economy and count as ‘broad money’ in the specification of the MONEY SUPPLY. See FINANCIAL SYSTEM.

built-in stabilizers see AUTOMATIC (BUILT-IN) STABILIZERS.

bulk-buying the purchase of raw materials, components and finished products in large quantities, thereby enabling a BUYER to take advantage of DISCOUNTS off suppliers’ LIST PRICES. A supplier may offer a price discount to encourage the placement of large orders as a means of obtaining extra sales in order to exploit fully the ECONOMICS OF SCALE in production and distribution. In many cases, however, the initiative lies with buyers, with powerful retailing and wholesaling groups exacting favourable price concessions from suppliers by playing one supplier off against another. See CHAIN STORE, OLIGOPSONY, MONOPSONY.

bull a person who expects future prices in a STOCK EXCHANGE or COMMODITY MARKET to rise and who seeks to make money by buying shares or commodities. Compare BEAR. See SPOT MARKET, FUTURES MARKET, BULL MARKET.

bullion precious metals, such as GOLD, silver, platinum, etc., that are traded commercially in the form of bars and coins for investment purposes and are used to produce jewellery and as industrial base metals. Some items of bullion, gold in particular, are held by CENTRAL BANKS and are used as INTERNATIONAL RESERVES to finance balance of payments imbalances.

bullion market a MARKET engaged in the buying and selling of precious metals such as GOLD and silver and gold and silver coins such as ‘Krugerrands’ and ‘Sovereigns’. The London Bullion Market is a leading centre for such transactions.

bull market a situation where the prices of FINANCIAL SECURITIES (stocks, shares, etc.) or COMMODITIES (tin, wheat, etc.) are tending to rise as a result of persistent buying and only limited selling. Compare BEAR MARKET. See SPECULATOR.

Bundesbank the CENTRAL BANK of Germany.

burden of debt INTEREST charges on DEBT that arise as a result of BORROWING by individuals, firms and governments. In the case of governments, interest charges on the NATIONAL DEBT are paid for out of TAXATION and other receipts. The term ‘burden’ would seem to imply that government borrowing is a ‘bad’ thing insofar as it passes on financial obligations from present (overspending) generations to future generations. The fundamental point to emphasize, however, is that the interest paid on the national debt is a TRANSFER PAYMENT and does not represent a net reduction in the capacity of the economy to provide goods and services, provided that most of this debt is owed to domestic citizens.